Inventory inventory 3 sample. Inventory inventory list: sample

Inventory inventory record - a form of a unified form of documentation, drawn up during the procedures for accounting for valuable property at a particular enterprise or organization. The procedure for filling in the inventory, the obligation to use it, the necessary details of the form are the main points that you must know in order to correctly record the results of the inventory.

Inventory inventory of goods and materials

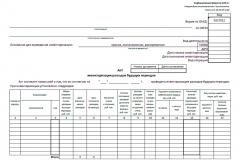

Inventory inventory of goods and materials, the INV-3 form is approved by the resolution of the State Statistics Committee of 08/18/1998 No. 88. Registration INV-3 is necessary for the purpose of fixing the actual availability of inventory in a particular organization. In this case, goods and materials are understood:

- products;

- finished products;

- production or other stocks of the company, etc.

Values \u200b\u200bcan be stored in specially designated places (warehouses, boxes, hangars, etc.) or located at any stage of the movement in connection with the activities of a legal entity. Thus, the information entered in the INV-3 form is determined during the ongoing recounting, weighing, and measurement procedures exclusively at the location of the goods and materials.

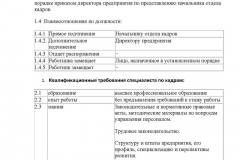

Mandatory details INV-3

When using the unified form of inventory during the inventory process, the employees of the inspection commission need to know what mandatory details are to be filled out. Inventory inventory INV-3 should contain:

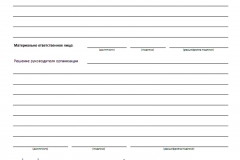

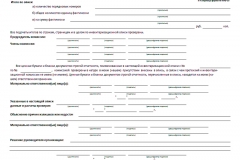

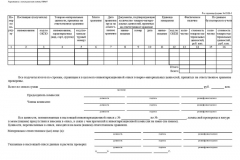

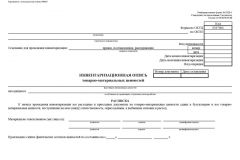

Inventory page 1 - receipt

Filling in the inventory begins with the introduction of the required details in the receipt:

- In the fields “Organization” and “Structural unit”, the full or abbreviated company name of the organization is entered in accordance with its constituent documents.

If the staffing division into the structural departments of the company is not provided, the corresponding field remains blank.

- The basis for the inventory is the internal administrative document of the executive body of the company (decision, order, order), the date of its preparation and registration number. The unnecessary name of the document shall be crossed out.

The frequency of inventories is determined by the leadership of a particular legal entity. The audit may be scheduled or carried out urgently. Inventory inventories of inventory during a planned inventory in their form and content are no different from those compiled during an unplanned inspection.

- In the fields “Date of the beginning of the inventory” and “Date of the end of the inventory” the calendar designations are entered corresponding to the time of the inventory activities.

- The document number and the date of its preparation are filled out in accordance with the organization’s current policy for maintaining and recording internal document circulation.

- In the column “Type of inventory” indicates the name of the goods or other industrial products subject to accounting.

- The next ordinal field should contain information about the type of ownership, on the basis of which jur. the person makes use or disposal of goods and materials - property, rent, storage, processing, etc.

- As materially responsible persons, the positions and personal data of employees who are entrusted with the maintenance of accounting and inventory of values \u200b\u200bare indicated. Such an obligation may be provided for by an employment contract, order, order, agreement on the assignment of duties for the safekeeping of goods and materials, job description, etc.

- At the end of the receipt, the actual date of withdrawal of the remaining goods is indicated.

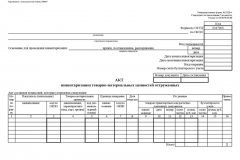

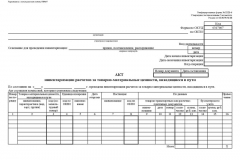

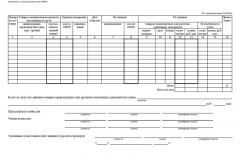

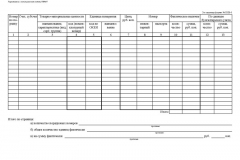

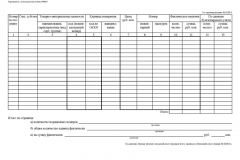

INV-3: sample filling 2-4 pages of inventory

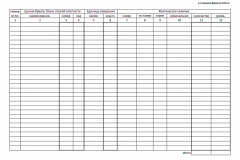

An inventory of inventory items (pages 2, 3, 4) is presented in the form of a table that includes the following information:

- account and sub-account numbers;

- name and information characterizing goods and materials;

- quantity of values, unit of measure, item number;

- unit cost of goods;

- information on the actually identified amount of inventories and on the reflected volumes according to accounting data.

The inventory of inventory items in the final line is filled, according to all information, numbers and amounts exclusively in words.

All members of the commission specially created for carrying out the inventory are signed with the form for the inventory inventory of inventory items. In addition, the inventory is certified by the signature or signatures of the employees materially responsible for the preservation of the valuables, and also endorsed by the chief accountant confirming the performance of the comparison operation.

Duty to use the document

The use of a unified form of inventory, beginning in early 2013, is not the responsibility of business entities. In order to comply with the rules of the law on accounting, organizations can use a self-developed form for inventory of inventory items. A sample of a self-developed form must contain the required details specified above. The exception is budgetary organizations, the obligation to use which a unified form of inventory is fixed at the legislative level.

Before starting the inventory of goods and materials, the initiator of the audit creates a special commission of the organization’s employees. The inventory inventory itself is compiled in hard copy in 2 copies: 1 is handed over to the accounting department to draw up the collation statement, 2 remains at the disposal of persons who are financially responsible.

In the event that the commission reveals goods that are not considered by the accounting department, all data on such inventories must be reflected in the inventory of material inventories.

For materials related to material assets, but having lost their properties for further use (damaged or unsuitable for production), relevant acts are drawn up.

From 01.01.2018, amendments to the Tax Code will come into force, according to which separate VAT accounting for goods (work, services) used both in taxable VAT and in non-taxable / tax-exempt operations will be necessary, even if the rule is observed five percent.

Inventory inventory list (sample)

The availability and reliability of information on inventory items (hereinafter also referred to as inventory materials) in the organization needs periodic verification (inventory). During the inventory, the fact of the presence of goods and materials is established and documents are drawn up with information about such goods and materials. One of such documents is an inventory according to the approved INV-3 form. Consider its content and the order of design.

Inventory of goods and materials

The inventory is preceded by the establishment of a list of workers who will conduct it (i.e., members and the chairman of the inventory commission), the deadline for the inventory and the reasons for it. This information is fixed by the order of the head (order form approved by the State Statistics Committee - form INV-22).

During the check, the following shall be included in the inventory list of inventory items:

- productive reserves;

- finished products;

- products;

- other stocks.

Information on how and what exactly needs to be inventory is contained in the Methodological instructions of the Ministry of Finance of the Russian Federation of June 13, 1995 N 49.

The inventory commission shall enter the information on inventories identified during the verification process into the INV-3 form specially provided for these purposes, which is called the “inventory inventory”.

Information on the actual availability of such values \u200b\u200bin the organization is entered in the specified document.

In particular, the following information should be contained in the inventory:

- name of values;

- view, group of goods and materials;

- the number of such values;

- variety, etc.

As follows from the Instructions of this state body, for all places of storage of the valuables under consideration and for each official who is responsible for them, a separate inventory is compiled in the form of INV-3.

This document is drawn up based on the results of the counting, weight determination, and measurement of inventory items carried out by members of the inventory commission.

If during the inspection low-quality goods and materials are found, relevant acts are drawn up in relation to them.

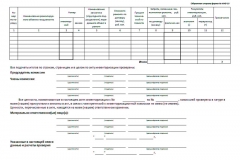

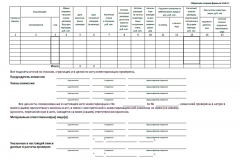

The unified form of the inventory list of inventory items consists of four pages.

The first page contains information about the organization, details of the order on conducting an inventory, as well as signatures of officials who bear the corresponding liability.

The second and third pages contain the inventory directly.

The fourth page contains the summary information and its supporting signatures.

It is necessary to fill in the INV-3 inventory in two copies (one of them must be sent to the accounting department, the other to the corresponding materially responsible official).

The legislation of the Russian Federation does not require the compilation of an inventory in accordance with the above INV-3 form.

On the contrary, according to Information of the Ministry of Finance of Russia No. ПЗ-10/2012, unified forms are not obligatory for enterprises and organizations. Therefore, organizations and enterprises have the right to develop and approve (with mandatory consideration of federal law) their form of an inventory of inventory items (a sample of such a form does not need any registration).

Sample of filling inventory inventory

The legislation of the Russian Federation on commercial activities implies the need to keep records of all material values.

The algorithm of this procedure is also established in special legislative norms.

Verification of compliance with the main points associated with such procedures is carried out by the Federal Tax Service.

Therefore, before proceeding with the implementation of this procedure, it is necessary to carefully familiarize yourself with all the nuances.

This will avoid a variety of difficulties and difficulties. And first of all, the appointment of a variety of fines for violation of the law.

Highlights

An inventory of inventory in a store or in another enterprise engaged in commercial activities is carried out taking into account certain important points.

A complete list of them is reflected in sufficient detail in special legislation. Moreover, it is important to remember the documentary support of such an inventory.

Verification of the relevant forms is carried out by regulatory authorities. There are also certain features of the procedure in certain segments of the activity.

These include an inventory of inventory in a pharmacy. There is a certain shelf life, as well as the storage of such goods.

Failure to comply with the rules can lead to quite serious troubles. Inventory allows you to solve a large number of different problems at the same time.

Before proceeding with the inventory procedure, you will need to consider the following issues:

- what it is?

- what is the role of the document;

- legal regulation.

What it is

First of all, it is necessary to deal with the very concept of “inventory”. The easiest way to do this is with a simple example.

You should also be aware of several types of inventory procedure itself. It can be carried out both because of the existence of such a requirement in legislative norms, and on other grounds.

Often an inventory is carried out by the owner of the enterprise in order to identify losses, determine the exact quantity of goods.

Another important point concerns the form of inventory. In accordance with legislative norms, it must be used in the established manner.

There are simply no alternatives. This moment is fixed at the legislative level. Only required to apply.

But this rule applies only to the inventory, which will subsequently be used for reporting.

Since INV-3 is precisely the reporting document. Required for financial statements.

In the event that the inventory process is carried out by the owner on his own initiative, the format for the reflection of information can actually be any other.

What is the role of the document

The role of this type of document is significant. Using the INV-3 form it is possible to solve a variety of problems.

Currently, this uniform form is used for the following purposes:

Moreover, this document allows not only to establish the fact of the presence of a certain quantity of goods.

In the future, after compilation, it can be requested for review by regulatory organizations. First of all, it is the Federal Tax Service.

There are also many other institutions that are also entitled to request reporting documentation.

Also, INV-3 is almost always compiled if a change of leadership is carried out, other reorganization actions take place at the enterprise.

Thus, the process of transferring property to another person is carried out. This moment has a large number of very different nuances.

It is important to avoid making mistakes when compiling such an inventory sheet. Since this can lead to quite serious problems later on.

Legal regulation

The format of the inventory sheet itself is reflected in a special version. The revision of 05/03/2000 is currently valid.

This document includes the following key points:

- the decision itself;

- unified format of accounting records - basic provisions, full

- a list of forms of accounting documentation of various types;

- establishes basic guidelines for use, as well as filling out certain formats;

- used and;

- what is an expense order;

- unified forms of documentation of the primary type:

| The moment is established regarding the inventory of fixed assets | |

| The format of the inventory label is indicated, how this document is compiled | |

| INV-3 | What is an inventory of commodity and material values |

| How is the inventory act compiled of already shipped material as well as commodity values | |

| The question is related to the inventory of goods that were previously transferred for safekeeping | |

| An act drawn up on material as well as commodity values \u200b\u200bthat are at a particular time in transit | |

| The act required to reflect fixed assets, the repair of which for some reason was not completed | |

| Future Expense Inventory Process | |

| Cash inventory process | |

| Inventory list of shares, as well as other securities falling within the indicated definition | |

| What is an inventory procedure order? |

- how is the inventory of fixed assets carried out - INV-1 second page, INV-1 third page;

- inventory of commodity and material values \u200b\u200b- second and third pages of INV-3, fourth page of INV-3.

This resolution reflects all the most significant nuances associated with both the compilation of INV-3 and the formation of other similar documents.

There are a large number of different nuances related directly to the preparation of an inventory. The person making this inventory should study them.

![]()

Making mistakes, descriptions in such statements is unacceptable. This can lead to serious fines by the Federal Tax Service, as well as other institutions.

How to fill in the form of inventory inventory

The process of compiling this form itself usually does not cause any significant complications. But it is important to follow the algorithm, format.

Today, specialized automated applications are usually used to compile such inventory lists.

This allows you to avoid errors at all or to reduce the likelihood of their occurrence to the very minimum. The main issues include:

- unified form INV-3;

- description of the species;

- signature example;

- sample fill;

- reflection by wiring.

Unified form INV-3

The unified INV-3 form is always compulsory at least in 2 copies.

Without fail, a signature must be affixed with decoding for the compilation of a document of persons.

The grounds for the signature are certain mandatory procedures:

- recalculation;

- weighing;

- mixing;

- recounting;

- other measurement procedures.

One of the copies must be transferred to compile a special statement for performing calculations.

The second copy must be kept by the person responsible for the preparation. This is necessary in case of any non-joining and in case you need to check.

When conducting an inventory procedure for goods that for some reason have been spoiled, a special one is taken.

The preparation of this type of document is provided both on paper and on electronic media. Filling is carried out in accordance with the requirements for standards of relevant documents.

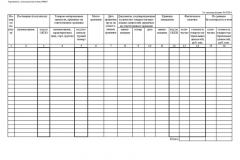

The statement itself is a table with 9 columns. The filling process itself is carried out in accordance with certain requirements.

View description

If there is no experience in compiling documentation of this format, you should carefully familiarize yourself with all the nuances in advance.

A sample document is not difficult to find on the Internet. It is important to use only reliable ones as a source.

Today, a document of this kind necessarily includes at least 4 pages. All of the designated required to be required.

Video: inventory of goods in stock

There are certain rules for compilation, filling. A complete list of such rules is reflected in the relevant regulatory documents.

It often happens that as a result of an inventory of material values, any that are not previously included in the inventory are revealed.

In this case, it is necessary to measure them or to perform other actions with them and conduct their inventory. Inventory with such commodity and material values \u200b\u200bis carried out as standard.

Signature Example

In a warehouse during a planned inventory, it is required to use the standard form of this document.

This type of document includes the following sections:

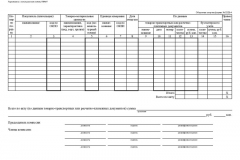

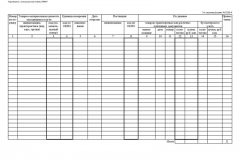

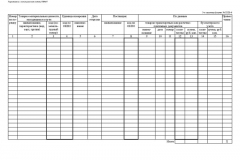

| Page number1 | name of organization and structural unit; grounds for the implementation of the inventory process; start and end date of the inventory; document number, as well as the date of preparation; further it is required to designate a receipt of responsible persons |

| Page 2 and 3 contains a table with the following columns | number in order; account, subaccount; commodity and material values, census - name, quantity; unit; price; passport and inventory number; actual availability; according to accounting |

| Page number 4 includes the following | “total” is indicated according to the results of the inventory; the full list of members of the inventory commission is indicated - necessarily with a breakdown; signatures and responsible for the implementation of the inventory procedure are indicated |

![]()

Sample fill

In the absence of a correctly compiled sample, it is worth using special automation programs to compile the INV-3 statement.

At the moment, the optimal solution is to use the 1C program. This service allows you to reduce the number of actions regarding filling out the sheet to the minimum.

Wiring Reflection

The inventory sheet should be reflected in the accounting entries.

For example, if there is excess material:

The process of compiling an inventory of the type in question has certain features. Having previously studied them, it will be possible to avoid making all kinds of typical mistakes.