Closing an un is as easy as opening it. How to close an individual entrepreneur with debts to the Pension Fund, tax and other debts - step-by-step instructions for self-liquidation Self-closing of an individual entrepreneur in a year

You can close the IP yourself without any problems with the step-by-step instructions below. Although you can periodically hear about the potential difficulties of this procedure, in reality everything turns out to be much simpler. In general, it all depends on the requirements tax office.

To close an individual entrepreneur with employees, a mandatory item before submitting documents is dismissal and settlement with employees, as well as submission of reports for them.

However, many tax authorities may not accept documents on deregistration of individual entrepreneurs and require them to complete the rest of the steps from the list before completing them. We can say that basically these requirements are illegal and in this case it is necessary to insist on the acceptance of documents, ignoring the "fake" tax threats.

You do not need to provide any certificates about the absence of debts to extra-budgetary funds to the tax office! This is an outdated procedure. Since 2011, the Federal Tax Service itself has been applying for this information to the funds.

Step-by-step closing of IP 2018

STEP 1 -

STEP 5 - Submission of documents to the tax

STEP 7 - Payment of all insurance premiums: "" and.

Closing a sole proprietorship with debts

In some tax offices, you can encounter "resistance" when you apply for the closure of an individual entrepreneur. Inspectors are starting to argue that it is impossible to close with debts and outstanding payments. At the same time, they refuse to accept documents. This is all nonsense.

1) Nowhere in the laws do they regulate the influence of debts, insurance premiums on the possibility / impossibility of closing an individual entrepreneur.

2) Debts, outstanding contributions and payments still remain with you, but already as an individual after deregistration.

Therefore, if you are faced with a refusal to accept documents for closing an IP because of your debt obligations, then just continue to stand your ground. The tax authorities themselves know that this can be challenged in court, and not in their favor.

Of course, the situation will become somewhat more complicated if, for example, you forgot about your individual entrepreneur for 5 years and did not pay at the same time insurance premiums... In such cases, arrears, fines, and penalties are usually charged. Through the courts, as a rule, it is possible to achieve the cancellation or reduction of arrears. But the main debt is not going anywhere anyway. And AGAIN: in a similar situation, they also have no right to refuse to close the sole proprietorship.

As already mentioned, the only thing when they can refuse to deregister an individual entrepreneur from the register and, moreover, justifiably, is if the individual entrepreneur has not submitted reports on his employees to the PFR, as well as if he has not made a dismissal and settlement with employees.

On many sites categorical articles are posted, allegedly with debts it is impossible to close an individual entrepreneur. This could be written either only by incompetent people in this matter, who themselves in practice did not close the IP, or who, upon refusal to enter the tax office, dutifully agreed to this, not wanting to defend their rights and thoroughly understand this issue.

If you still doubt whether it is possible to close an individual entrepreneur with debts, go to any forum on this topic: people write in black and white that they did it. And some with amounts of debt "above the roof".

Various life circumstances sometimes force an entrepreneur to stop his activity. In order to avoid unnecessary problems, it is necessary to comply with the procedure for closing an individual entrepreneur provided for by law. This procedure is no more difficult than the main thing is to know what to do and how to do it.

Deregistration of individual entrepreneurs in the tax office in 2016

Termination of entrepreneurial activity natural person is subject to mandatory registration with the Federal Tax Service of Russia. In practice, situations often arise when an individual entrepreneur believes that he is no longer an entrepreneur only on the grounds that he does not conduct commercial activities. An additional reason for this may be the closure of the current account, the destruction of the seal. However, all these actions are not documentary evidence of the IP liquidation. Status individual entrepreneur is removed from the citizen only after making the appropriate entry in the United State Register individual entrepreneurs. This procedure is carried out only after the submission of a certain package of documents.

Step-by-step instructions for closing an individual entrepreneur in 2016

It is much easier to terminate the activity of an individual entrepreneur than. An individual entrepreneur must submit a minimum package of documents to the tax authority at the place of residence and receive a Termination Certificate in five working days. From this moment, the IP is considered officially closed.

But before submitting documents to the tax office, you must perform a number of actions:

- make settlements with counterparties;

- close the current account;

- dismiss employees - they must be notified of the upcoming termination of activities at least two months in advance;

- notify the licensing authorities of the termination of activities - surrender licenses and other permits if they were received for the implementation of the activity;

- prepare and submit all reports to non-budgetary funds and tax authorities;

- destroy the seal.

Only after completing these steps can you contact tax authorities with a statement to close the IP. Note that if the individual entrepreneur did not have employees, then this preparatory process would not take much time.

Documents for closing an individual entrepreneur in 2016

To terminate activities as an individual entrepreneur, the following documents are required:

- an individual's passport;

- application form R26001;

- a receipt for payment of the state fee.

The application can be completed with a ballpoint pen or typewritten. There is nothing difficult in filling it out. It is required to indicate only: last name, first name, patronymic, as well as TIN and OGRNIP. The application form can be downloaded from the official website of the tax office or from any reference and legal system.

Both the entrepreneur himself and any other person under a notarized power of attorney can submit an application to the tax office. Also, the legislation provides for the possibility to send an application by mail. In this case, it must be sent by registered mail with a list of attachments. This option allows you to close the IP while in another city. Another option for filing documents for the termination of activities is through a special service on the FTS website.

The term for consideration of the application and making an entry in the USRIP is five working days. Thereafter, the former entrepreneur must come to obtain a Certificate of Termination. If within the specified period he does not receive this document, then tax office will send the original of the certificate to the place of registration by registered mail.

Sometimes situations arise when an entrepreneur has not received this certificate, in which case he has the right to apply to the Federal Tax Service with an application for the issuance of a certificate or its duplicate, or he can simply request a certificate that he does not have registration as an individual entrepreneur.

Receipt for the state duty for the closure of an individual entrepreneur in 2016

To terminate the activity of an individual entrepreneur, you must pay a state fee. In 2016, its size is 160 rubles. In order to avoid mistakes, it is best to generate a receipt for payment on the website of the tax office. You can pay for it at any branch of the bank, as well as through personal accounts online banking. Payment is also allowed for the entrepreneur's current account, if it has not yet been closed by the time the documents are submitted. By the way, the legislation does not contain any restrictions on the date of payment of the state fee, so it can be paid even six months before closing.

The application for the termination of activities is accompanied by the original receipt of the payment made.

Declaration at the closure of the sole proprietor in 2016

The closure of an individual entrepreneur does not relieve the obligation to provide reports for the period of entrepreneurial activity, even if, in fact, it was not conducted. The reporting procedure depends on the taxation system. For example, a declaration under the simplified taxation system will need to be submitted by the 25th day of the month following the month of termination of activities. An entrepreneur has the right to submit a report on the simplified tax system even before the application for resigning from the status of an individual entrepreneur is submitted. This is especially true if the activity has not been conducted for a long time, therefore, a "zero" report submitted simultaneously with the filing of liquidation documents will avoid an unnecessary visit to the tax office. An entrepreneur working on UTII must report before closing, this is due to the specifics of this tax regime.

If the entrepreneur had hired workers, then before the closure of the individual entrepreneur, it is necessary to submit all reports on them to the Pension Fund, Fund social insurance, report on personal income tax.

In addition, if the entrepreneur has cash register, it is necessary to deregister it and submit a Z-report. The entrepreneur himself can keep the CA or sell it.

Advice: if the entrepreneur has real estate that he uses for business purposes, which he plans to sell, then it is advisable to do this before the termination of the activity. In this case, sales tax will be calculated depending on the tax system used. For example, income on the STS is 6%. When selling this property as an individual, you will have to pay 13%.

How to close an individual entrepreneur with debts in 2016 - step by step instructions

In some cases, debts become the reason for the closure of individual entrepreneurs. Liabilities can arise both to creditors and to government agencies: tax, PFR, FSS.

In practice, there are often situations when the decision to officially terminate activities as an individual entrepreneur is made after the initiation of enforcement proceedings in respect of arrears of mandatory contributions to the Pension Fund. Previously, this debt prevented the closure of individual entrepreneurs - the tax authorities demanded from the entrepreneur a certificate of the absence of debt to the Pension Fund of the Russian Federation. Currently, some tax authorities are still requesting this document, but the presence of debt cannot serve as a basis for refusing to register the termination of activities.

There is no legal prohibition on closing an individual entrepreneur in the presence of debt, including to the budget and extra-budgetary funds, therefore, officially terminate entrepreneurial activity it is possible with debts. Refusal to register the termination of activities may be appealed against in court. But it should be remembered that even the removal of the status of an individual entrepreneur does not exempt from obligations arising in the course of entrepreneurial activity. Therefore, a citizen who was previously an entrepreneur will have to pay off all the debts that arose when he was an individual entrepreneur. Moreover, he is responsible for these debts in full, this rule applies to all credit obligations of the entrepreneur.

It is worth paying attention to the fact that if the entrepreneur received, then it may be necessary to return the funds received to the state. Judicial practice shows that in a number of cases, the bodies of state support for business through the court obliged entrepreneurs to return the funds for material support if they became aware of the termination of entrepreneurial activity. The specific conditions for the return of subsidies upon closing the IP depend on the features of the program and the goals of support.

In some situations, it is more profitable to terminate the activity of an individual entrepreneur through bankruptcy proceedings. In this case, the following conditions must be met:

- delay in mandatory payments and other financial obligations is three or more months;

- the amount of debt exceeds the value of the entrepreneur's property;

- the total amount of debt exceeds ten thousand rubles.

The initiator of the bankruptcy procedure can be both the entrepreneur himself and his creditors, as well as government bodies... However, it should be borne in mind that this procedure will require certain cash, and the procedure itself can take a long time.

How much does it cost to close an individual entrepreneur in 2016

The cost of closing an IP depends on the specific circumstances of the termination. So, if an entrepreneur independently deals with all issues of termination of activities, then his expenses will be reduced to paying a state fee in the amount of 160 rubles. When contacting a legal company, closing an individual entrepreneur will require from 1000 to 3500 rubles.

Also, the costs of terminating business activities can include the costs of settlements with personnel, counterparties, as well as the payment of taxes and fees. Each entrepreneur has a different size. It is necessary to take into account that if an entrepreneur conducted activities independently, then he must, within 15 days from the date of termination of activities, pay a fixed contribution to the Pension Fund of Russia for the period worked in the current calendar year. Payment of contributions and taxes from employees, however, must be carried out before the closure of the individual entrepreneur.

Consequences of IP closure

After the termination of registration as an individual entrepreneur, a citizen is no longer entitled to carry out entrepreneurial activities. But the law allows him to register again as an individual entrepreneur at any time, so anyone can short time get the organizational and legal registration for implementation. Moreover, you can open a new IP the next day after receiving the closing documents. There are only a few exceptions:

- a citizen is disqualified by a court decision - for a period of disqualification;

- the IP is declared bankrupt - within one year from the date of the court decision;

- other grounds that, according to the law, prevent a citizen from registering as an individual entrepreneur, arising after the termination of the status of an individual entrepreneur.

In life, situations often arise when a citizen has officially ceased entrepreneurial activity, and after a short time again decides to open an individual entrepreneur. For example, he found the option profitable business who can, therefore, he needs to become an entrepreneur again.

Advice: in some cases, it may be beneficial to close and re-enter the sole proprietorship. For example, in order to receive some subsidies, the life of an IP must be minimal, and the fact of reopening in this case does not matter.

Save the article in 2 clicks:

You can always stop working as an individual entrepreneur. The law does not contain grounds that would prevent this from being done. Moreover, the closing procedure takes a minimum of time, and in most cases does not require serious financial costs. At the same time, the closure of the IP does not make it impossible to open it again when the need arises. For example, it can be implemented only by an officially registered business entity. Therefore, both a beginner and a former entrepreneur should always remember that it is always possible to become an individual entrepreneur, including after a voluntary closure.

In contact with

Hello! There are many reasons for individual entrepreneurs to stop their business activities. Sometimes these reasons are compelling enough to even with debts. In a broad sense, liquidation can be voluntary or compulsory - depending on the initiator (the entrepreneur himself or the court), but in both cases there are special cases. We will talk about this in this article!

Possible reasons for closure

Here are the most common situations as an example:

- Personal decision of the entrepreneur... Under this point lies a lot of situations - from loss of interest in the case to moving to another city or changes in the personal life of an individual entrepreneur. You are not required to indicate the reason for the closure anywhere, if you do it of your own free will.

- Bankruptcy... When there are too many debts, and the individual entrepreneur realizes that he does not have enough funds to pay them off, the most correct decision becomes.

- Compulsory liquidation by court decision(as a measure for serious violations and debts).

- Loss of citizenship or invalidation of a document authorizing a foreign citizen to reside and operate on the territory of the Russian Federation.

- Death of an individual entrepreneur.

Features of closing IP with debts

Sooner or later individual entrepreneurs cease their activities, and then the liquidation procedure begins, or, in other words, the closure of individual entrepreneurs.

The liquidation of an individual entrepreneur can be voluntary or compulsory., in any case, this procedure is quite simple and quick. However, if at the same time the individual entrepreneur has unpaid debts to funds, employees or partners, additional questions and doubts - will everything go as smoothly as we would like?

Step-by-step instructions for liquidating individual entrepreneurs with debts

To close the activities of an individual entrepreneur with debts, you will have to perform a number of actions:

Step 1: Close tax debts and submit reports. An application for the liquidation of an individual entrepreneur will not be accepted if at that moment you have debts to the tax office. But with debts to the Pension Fund and the Social Insurance Fund, according to the legislation for 2016 - 2019, you can pay off after the liquidation of the individual entrepreneur. The tax office does not have the right to demand from you a certificate of repayment of debts to funds. But this debt cannot remain unpaid, and if necessary, it will be filed for collection through the court. The same applies to debts to employees and partners.

Step 2: Pay at any branch of Sberbank the state duty for liquidation (160 rubles).

Step 3: Collect the necessary documents and submit them to the registration authority:

- Passport and copies of its pages;

- Copies of the certificate, certificate of tax registration and extracts from USRIP (indicating OKVED);

- Notarized statement of business closure (form Р26001);

- Receipt of payment of the duty.

Please note that you need to apply for the liquidation of an individual entrepreneur in the same department where you registered as an individual entrepreneur, and not where you were registered. The documents can be taken in person, through a trusted person (in this case, you will need a notarized power of attorney) or by registered mail with an inventory and declared value.

Step 4: There is no need to notify the PFR and FSS about the termination of activities, they will receive a message automatically from the tax office. But if you wish, you can play it safe and send them a free-form notification, since there are no approved forms for this case.

Step 5: After five working days, return to the tax office for a certificate of termination commercial activities and an extract from EGRIP.

Step 6: at the bank (if he was) - for this, come to the bank branch and write an application.

Step 7: If, before submitting an application to the tax office, you have not submitted all the declarations, then it is necessary to do this, as well as to submit the final tax return for the calendar year, no later than 5 days after the confirmation of the tax closure of the individual entrepreneur. For the remaining omissions before the tax office, you may be charged penalties and fines.

Outstanding debts threaten individual entrepreneurs with an increase in debt, a lawsuit and collection (sometimes with a sale of property).

For example, if an individual entrepreneur still has a debt to the Pension Fund, he is obliged to pay it even after the business is liquidated. The FIU has the right to collect debts through bailiffs, then you will have to pay another plus 7% of the debt.

When can I reopen the IP

If you closed the IP by own initiative and have already paid off all debts, then at any time you can again. As for the compulsory liquidation, the term of the ban on doing business is indicated in the court decision.

Bankruptcy as a way to liquidate individual entrepreneurs with debts

If the entrepreneur does not have enough funds to pay off all debts ( total amount which, according to the law, must be at least 500,000 rubles), and the liquidation of an individual entrepreneur from obligations on debts does not relieve - we have already spoken about this earlier - then instead of closing an individual entrepreneur, it is more expedient to file for bankruptcy.

These are completely different procedures, and in the case of bankruptcy, file a package required documents will have to go to the arbitration court, which itself will later transfer the information to the tax one, and the individual entrepreneur will be liquidated automatically. You will be able to re-become an individual entrepreneur no earlier than in five years.

In conclusion, we note once again that it is possible to liquidate an individual entrepreneur with debts, and this is quite easy to do. All debts - except for the tax debt - can be repaid after the liquidation of the individual entrepreneur, but in the event of a deviation from payment, the former individual entrepreneur faces penalties and litigation.

Relations arising in connection with the state registration of individuals as an individual entrepreneur, as well as in connection with the termination of activities as an individual entrepreneur, are regulated by the Federal Law of 08.08.2001 No. 129-FZ "On state registration legal entities and individual entrepreneurs ”.

How long does it take to pay insurance premiums upon termination of the sole proprietorship?

In accordance with Art. 432 of the Tax Code of the Russian Federation, payment of insurance premiums by payers who have ceased to carry out activities as an individual entrepreneur is carried out no later than 15 calendar days from the date of making an entry in the USRIP about the termination of entrepreneurial activities.How much should the fees be paid upon termination of the sole proprietorship?

Clause 5 of Article 430 of the Tax Code of the Russian Federation establishes that if payers stop carrying out entrepreneurial or other professional activity during the billing period, the corresponding fixed amount of insurance premiums payable by them for this settlement period, is determined in proportion to the number of calendar months for the month in which the state registration of an individual as an individual entrepreneur became invalid.For an incomplete month of activity, the corresponding fixed amount of insurance premiums is determined in proportion to the number of calendar days of this month until the date of state registration of the termination of an individual's activity as an individual entrepreneur (Letter of the Ministry of Finance of February 7, 2017 N BS-3-11 / [email protected]).

How long does it take to file a 3-NDFL declaration upon termination of an individual entrepreneur's activities?

A taxpayer is obliged to submit a declaration within five days from the date of making an entry on state registration when an individual stops acting as an individual entrepreneur in connection with his decision to terminate this activity in USRIP and deregister him from the tax authority as an individual entrepreneur (including for the period between the day of submission of an application for state registration of termination of activity as an individual entrepreneur and the day of exclusion of this entrepreneur from the USRIP) (clause 9 of article 22.3 Federal law of August 8, 2001 N 129-FZ, paragraphs 10 and 11 of Article 227 of the Tax Code of the Russian Federation, paragraph 3 of Art. 229 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance dated January 13, 2016 N BS-4-11 / [email protected]).Is there a penalty for late submission of a zero 3-NDFL declaration upon termination of the individual entrepreneur's activities?

If an individual entrepreneur, upon termination of activity, did not submit a declaration in the form of 3-NDFL to the tax authority in a timely manner, then the tax authority has the right to impose a fine of 1000 rubles. for late submission of reporting (zero) (clause 1 of article 119 of the Tax Code of the Russian Federation).Do I need to notary the signature of the person on the application for state registration of termination of activities as an entrepreneur?

It depends on how you submit documents to the tax office.The signature on the application does not need to be certified in the following cases:

- if the applicant submits documents directly to the Inspectorate of the Federal Tax Service and at the same time presents a passport or other identity document;

- if the applicant submits documents through Multifunctional Center, presents a passport (another identity document) and signs an application in the presence of an employee of the multifunctional center;

- if the applicant submits documents through single portal state and municipal services.

Do I need to notify the tax inspectorate and funds about the closure of the current account when the individual entrepreneur ceases to operate?

There is no need. Since May 2014, the obligation of organizations and individual entrepreneurs to report the opening and closing of bank accounts to the tax office has been abolished (Articles 5 and 6 of the Federal Law of 02.04.2014 N 59-FZ).What documents must be submitted to the Inspectorate of the Federal Tax Service upon termination of an individual entrepreneur's activities?

State registration upon termination of an individual's activity as an individual entrepreneur in connection with his decision to terminate this activity is carried out on the basis of the following documents submitted to the registering authority:a) an application for state registration signed by the applicant in the form R26001;

b) a document confirming the payment of the state fee (160 rubles);

c) a document confirming the submission to the Pension Fund of the Russian Federation of personalized accounting information, as well as information on additional insurance contributions for the funded part of the labor pension (Article 22.3 of the Federal Law "On State Registration of Legal Entities and Individual Entrepreneurs" of 08.08.2001 N 129-FZ) ...

Do I need to notify the FIU about the IP closure?

The entrepreneur himself does not need to send any notification to the FIU about the closure of the IP. The IP closure documents are transferred to the tax office, the tax authorities exclude the IP from the USRIP and they themselves transfer information to the FIU that such an IP is no longer listed in the register (clause 2 of article 11 of the Law of 12/15/2001 No. 167-FZ).Within how many days, from the date of submission of documents on the termination of the individual entrepreneur's activities, the tax office will deregister the entrepreneur?

According to paragraph 8 of Art. 22.3, paragraph 1 of Art. 8 of the Federal Law of 08.08.2001 N 129-FZ, state registration, upon termination of an individual's activity as an individual entrepreneur, is carried out within no more than five working days from the date of submission of documents to the registering authority.By virtue of paragraph 9 of Art. 22.3 of the Registration Law, the state registration of an individual as an individual entrepreneur becomes invalid in connection with the adoption by this person of a decision to terminate entrepreneurial activity after making an entry about it in the USRIP.

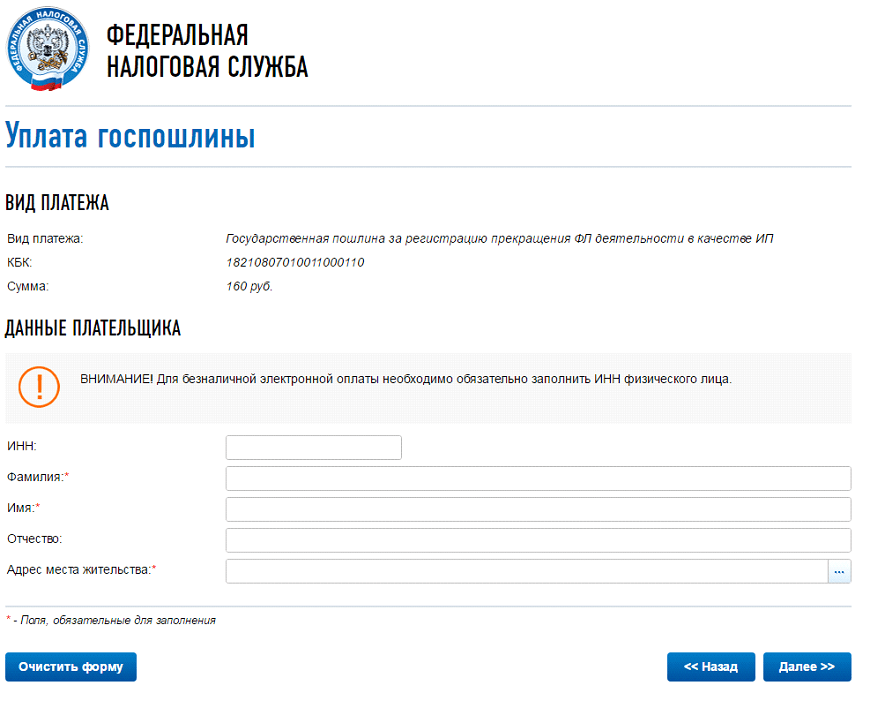

In what ways can you pay the state fee?

The state duty for closing an individual entrepreneur in 2017 is 160 rubles.There are two ways to get a receipt and deposit funds:

- Download a receipt of the state duty for closing an individual entrepreneur and appear at a bank branch to pay it;

- Across payment system online, which will automatically issue a sample of the state duty for closing an individual entrepreneur with the entered details of an individual.

In order for the fee for closing an individual entrepreneur to be paid, select the item "State duty for registering the termination of an individual entrepreneur as an individual entrepreneur", and then click "Next".

We fill in the fields. In the item "Address of residence", an additional window will open, there fill in everything according to the instructions and then the button "Next"

Check again all your data and choose how you will pay the state duty: "cash payment" or "non-cash payment".

If we choose "non-cash payment", then we are warned that non-cash electronic payments can only be made by clients of partner banks who have current accounts in them. You need to choose a bank and make a payment.

The sole proprietor ceased operations on April 12, 2017. Do I need to pay UTII for April?

Yes, you have to pay for 11 days in April. Clause 10 of Article 346.29 of the Code determines that the amount of imputed income for the quarter during which the taxpayer was deregistered in connection with the termination of business activities subject to the single tax is calculated from the first day of the tax period until the date of deregistration with the tax authority specified in notifying the tax authority about the deregistration of an organization or an individual entrepreneur as a single tax payer.If the deregistration of an individual entrepreneur in the tax authority as a taxpayer of UTII was made not from the first day of the calendar month, then the amount of imputed income for this month is calculated based on the actual number of days of the individual entrepreneur's entrepreneurial activity (Letter of the Ministry of Finance dated April 8, 2016 No. N SD-3-3 / [email protected], para. 3 p. 3 art. 346.28 Tax Code of the Russian Federation).

SP on UTII was deregistered as a taxpayer on March 25, 2017. Do I need to submit a UTII declaration for the first quarter of 2017?

Clause 3 of Article 346.32 of the Code determines that tax declarations for UTII based on the results of the tax period are submitted by taxpayers to the tax authorities no later than the 20th day of the first month of the next tax period.The Code does not provide for any peculiarities in the timing of submission of a tax return for UTII in the event that a taxpayer stops an activity subject to UTII and is deregistered as a UTII taxpayer or an individual entrepreneur.

Since the individual entrepreneur was deregistered as a taxpayer of UTII on March 25, 2017, he had to submit a tax declaration for UTII for the first quarter of 2017 no later than April 20, 2017, calculating in it a single tax for the actually worked period of time (from January 1 to March 24, 2017) (Letter of the Ministry of Finance dated April 8, 2016 N SD-3-3 / [email protected]).

Is the tax authorities entitled to conduct a tax audit after the closure of an individual entrepreneur?

The tax authorities have the right to conduct tax audits of entrepreneurial activities of individuals who, at the time of the audit, ceased these activities and lost the status of individual entrepreneurs (Definitions of the Constitutional Court of the Russian Federation of 25.01.2007 N 95-О-О, of 26.05.2011 N 615-О-О) ...The tax authority within the framework of the cameral tax audit has the right to demand explanations from the taxpayer if contradictions are found in the taxpayer's documents and (or) inconsistencies in the information provided by the taxpayer with the information available to the tax authority (clause 3 of article 88 of the Tax Code of the Russian Federation). The form of the requirement for the provision of explanations is given in Appendix No. 1 to the Order of the Federal Tax Service of Russia dated 05/08/2015 No. ММВ-7-2 / [email protected] The requirement should indicate what the errors and contradictions are.

A taxpayer who fulfills the requirement has the right to submit documents confirming the accuracy of the information reflected in the declaration (clause 4 of article 88 of the Tax Code of the Russian Federation).

Federal Law of 05/01/2016 N 130-FZ from January 1, 2017 for failure to submit, within a five-day period, the explanations requested in accordance with clause 3 of Art. 88 of the Tax Code of the Russian Federation, in case of failure to submit set time the revised tax return clause 1 of Art. 129.1 of the Tax Code of the Russian Federation introduces liability in the form of a fine in the amount of 5,000 rubles. (for a repeated violation within a calendar year - 20,000 rubles) (clause 2 of article 129.1 of the Tax Code of the Russian Federation).

Failure to submit documents to the tax authorities by the taxpayer in due time shall result in a fine of 200 rubles. for each non-submitted document (clause 1 of article 126 of the Tax Code of the Russian Federation, Determination of the Constitutional Court of the Russian Federation of November 20, 2014 N 2630-О). The tax authority has the right to demand documents during a desk tax audit only in cases provided for by tax legislation, which does not contain as a basis for requesting documents within the framework of a desk tax audit, a tax return paid when applying the simplified tax system, identification of contradictions by the tax authority in the documents submitted by the taxpayer ( information).

Should an individual entrepreneur on the simplified tax system, who has lost the status of an entrepreneur, separately submit to the tax authority a notice of the termination of entrepreneurial activity in respect of which the simplified tax system was applied?

No, you shouldn't. In the letter of the Ministry of Finance of Russia dated July 18, 2014 N 03-11-09 / 35436, communicated to the lower tax authorities and taxpayers by the letter of the Federal Tax Service of Russia dated 04.08.2014 N GD-4-3 / [email protected] it is said that according to general rule the loss of the status of an individual entrepreneur applying the simplified tax system means the simultaneous termination of the taxation system.Such taxpayers do not have the obligation to submit to the tax authority a notice of termination of entrepreneurial activity in respect of which the simplified taxation system was applied (Letter of the Ministry of Finance of April 8, 2016 N SD-3-3 / [email protected]).

The individual entrepreneur on the simplified tax system ceased operations (deregistered as an entrepreneur) on April 11, 2016. A notice of termination of business activities, in respect of which the STS was applied, was not submitted. What is the deadline for filing a tax return for 2016?

Since the individual entrepreneur ceased activities as an individual entrepreneur on 04/11/2016 and the notification of the termination of business activities, in respect of which the simplified tax system was applied, was not submitted, then he has no grounds for applying the provisions of paragraph 2 of Article 346.23 of the Code.Tax returns under the simplified tax system for 2016 must be submitted by an individual entrepreneur in accordance with the generally established procedure, i.e. no later than April 30, 2017. (Letter of the Ministry of Finance dated April 8, 2016 No. SD-3-3 / [email protected]).

Do I need to pay taxes when an individual stops working as an individual entrepreneur?

In accordance with paragraph 1 of Article 3 of the Tax Code of the Russian Federation, each person must pay legally established taxes and fees. By virtue of paragraph 1 of Article 45 of the Code, the taxpayer is obliged to independently fulfill the obligation to pay tax, unless otherwise provided by the legislation on taxes and fees.The grounds for the termination of the obligation to pay tax and (or) due are specified in paragraph 3 of Article 44 of the Code.

The termination of an individual's activity as an individual entrepreneur is not a circumstance that entails the termination of the obligation to pay tax arising from the implementation of such activity.

A taxpayer, in accordance with Article 64 of the Tax Code of the Russian Federation, may be provided with a deferral or installment plan for the payment of tax if there are grounds provided for by this article. An application for a deferral or installment plan for the payment of tax is submitted by an interested person to the appropriate authorized body (Letter of the Ministry of Finance dated August 4, 2016 N 03-02-08 / 45681).

How to recalculate the amount of tax under the PSN, if the individual entrepreneur ceased his entrepreneurial activity, in respect of which the patent taxation system was applied, before the expiration of the patent?

If an individual entrepreneur has ceased entrepreneurial activity, in respect of which the patent taxation system was applied, before the expiration of the patent, the tax period is the period from the commencement of the patent until the date of termination of such activity specified in the application submitted to the tax authority in accordance with paragraph 8 of Article 346.45 of the Tax Code RF.If, when recalculating, an individual entrepreneur who has paid the previously calculated amount of tax within the time limits established by paragraph 2 of Article 346.51 of the Code, appears:

- overpayment of tax, then he has the right, by submitting an appropriate application, to return or offset it against payment of other taxes in the manner prescribed by Article 78 of the Code;

- the amount of tax to be paid, then based on the current norms of the Code, the calculated amount of tax is not subject to payment late specified in the patent (Letter of the Ministry of Finance dated May 25, 2016 N 03-11-11 / 29934).